Hay varios factores que nos hace pensar que las cosas se están yendo de madre… Hay mucha liquidez en el sistema, de ahí que los bonos estén dando rentabilidades negativas en muchos sitios. Encima, va a haber más liquidez. Ya sabes que a partir del 1 de marzo se ha puesto en marcha el QE en Europa (60.000 mill euros al mes). En EEUU, la alternativa a invertir en renta fija con poco rendimiento es en acciones. Y siguen y siguen, rectilínea tendencia desde hace 7 años. Y eso que este año les va a pesar, ya que las subidas de los beneficios empresariales no son tan buenas…

Esta locura de compras y compras sin recortes, muy atípica, se mantiene… Aunque deberá haber recortes. El año pasado hubo tres fases correctivas de un 10% más o menos, en agosto, al final de septiembre, y en noviembre, pero se volvió arriba con rapidez… Es probable que la primera corrección la tengamos en junio, aunque no sería descartable que se adelantara…

El problema: no hay alternativa a donde invertir, a qué hacer con el dinero… Antes se tenía en depósitos cobrando una renta, ahora ya no…, ni en España ni en otros países.

Reasons to worry about US equities

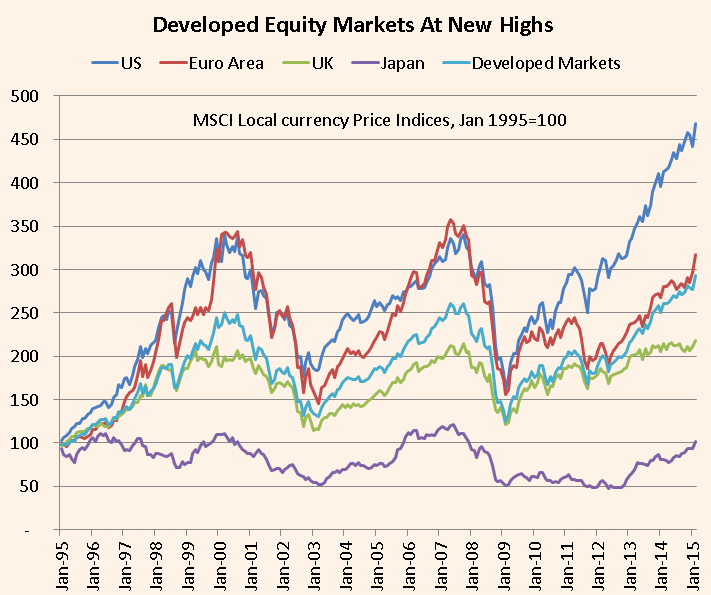

February was another very strong month for global equities, with the US market enjoying its best month since October 2011. Global equities are now up by 5.1 per cent this year, exceeding even the heady pace of the 2012-14 advance, though this time the Eurozone (+ 14.7 per cent) has outpaced the US (+ 2.2 per cent).

Once again, the pessimists have been confounded. The US market has now tripled since 2009, and has risen in a virtually straight line for over three years. The analyst community on Wall Street remains almost uniformly bullish about US stock returns in 2015. Although cynics will say “they always are bullish, that is what they are paid for”, many other indicators point to extremely positive market sentiment, with active equity investors generally positioned for further upside. And the VIX measure of equity volatility, a gauge of investor concern, is languishing near its long term lows at about 13.

Has the US market finally reached the point of over-exuberance? As Warren Buffetreminds us this weekend, market timing is always difficult, and it is particularly difficult to pick the top of a rampant bull market. But there are certainly increasing grounds to worry about the sustainability of the market’s advance in the rest of this year.

The global equity bull market, at least in the advanced economies, has been driven by two key fundamentals – a moderate but continuous recovery in real GDP and corporate earnings, and aggressively easy monetary policy. Because the US has been at the forefront of both these phenomena, the S&P 500 has vastly out-performed the global market for 6 successive years.

Both of these key fundamental drivers are now less convincing than before. US real GDP growth has slowed to around 3 per cent currently, compared to about 4 per cent in mid 2014, according to recent “nowcasts”. This, in itself, is not worrying, since the slowdown represents a return to a sustainable growth path after temporary factors boosted growth in mid 2014. The growth rate has been steady in the past couple of months and, although some data releases have disappointed economists’ optimistic forecasts, there is no evidence of a serious slowdown in the economy.

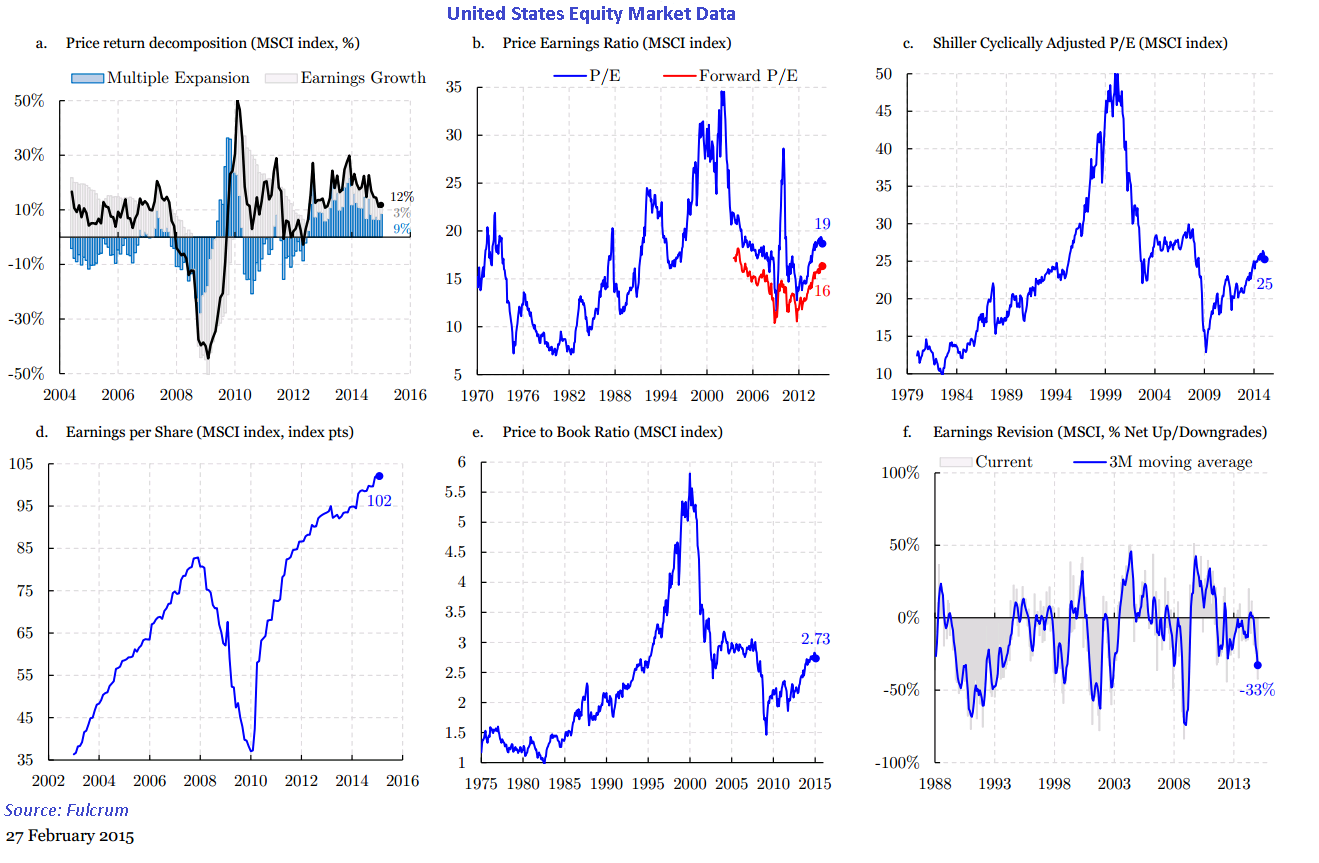

Corporate earnings are, however, being hit by the collapse in oil prices and the rising dollar. Albert Edwards, the market’s favourite bear at Societie Generale, wrote last week that the rate of decline in analysts’ forward profit expectations in the US is clearly associated with recession. According to MSCI data, profits downgrades are exceeding upgrades by a net 33 per cent at present – see the graph on the bottom right:

Much of the profits gloom is due to the oil crash, but we are not yet seeing any significant upward momentum in non oil profits, which is disappointing, given the strength of consumer spending. Based on past history, the 12 per cent rise in the dollar seen since early 2014 might reduce US corporate earnings by about 6 per cent, which explains why non oil profits have been lacklustre. A more serious decline in profits growth would occur if wage growth began to erode net margins, which are near all time highs, but that has not happened yet.

With overall profits growth decelerating to low single digit rates, about three-quarters of the rise in US equity prices in the past 12 months has been due to a rise in the market’s price/earnings ratio (ie “multiple expansion”). This has taken market valuations into fairly expensive territory compared to long term history, though this has not been at all unusual in the period since the mid 1990s, when P/E ratios and price/book ratios have been generally much higher than in prior decades.

One reason for these “expensive” valuations is of course the behaviour of the central bank. That, too, may be changing. Last week, Fed Chair Janet Yellen gave notice that the FOMC will probably remove its promise to be “patient” in March, raising the possibility of lift-off in short term interest rates in June or (she hinted) “soon” thereafter. Judging from her language, the choice for lift off is now between the June, July and September meetings. Pricing at the front end of the money market is currently split fairly evenly between these three dates.

Although this year’s lift off will be one of the most telegraphed moves in the history of the Fed, the reality of rising US rates could still spook an over-extended bond market. Lately, investors have pushed yields to new lows, on the theory that “there are not enough bonds in the world for the central banks to buy”. It is not clear that this mood will survive the first Fed rate increase, though a major bear market in bonds would be a surprise, given the extent of bond purchases by the ECB and Bank of Japan.

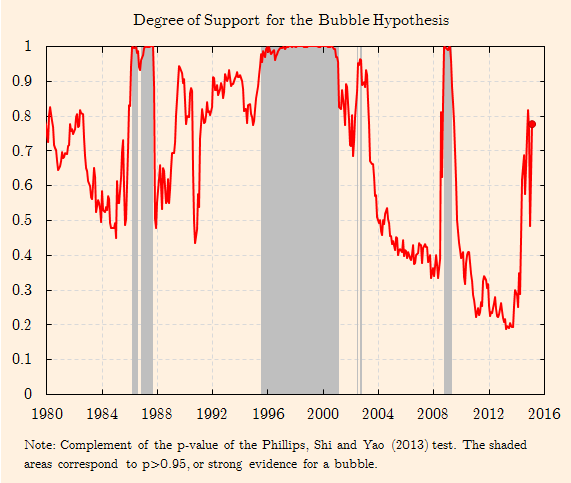

Neither the profits outlook, nor the central banks, are in themselves deteriorating enough to kill the bull market. But we also need to take account of the price action in the market itself. This blog has previously discussed an econometric model designed to judge the probability of an equity bubble, taken from a research paper by my colleagues. A bubble is detected by a sudden, explosive change in the price of equities, compared to the long run path of corporate earnings (ie the “Shiller P/E).

{kind=link}

{kind=link}

{kind=link}

The latest readings from the model are shown in the final graph. Although there was much loose talk about an equity “bubble” in both 2013 and 2014, the model detected a fairly low probability that one was occurring. For most of that period, it reported a probability of 20-40 per cent that a bubble was underway.

However, the recent sharp rise in the S&P 500, relative to earnings, has raised the probability that we may be entering a bubble. This probability has still not exceeded the key confidence threshold of 95 per cent so, strictly, the verdict of the model is “no bubble”. But in February, the probability rose to 78 per cent, which is not negligible.

Equity price action has therefore been unusually buoyant at a time when some key fundamentals are not as supportive as they have been for several years. Increased caution may be warranted for a while.

Abrazos,

PD1: Según DWS, hay flujo fuerte hacia las bolsas europeas:

¿Es consistente? Entre junio 2013 y junio 2014 lo hubo y subieron… Pero será algo de pocos meses, o habrá recurrencia???

Las expectativas económicas están cambiando hacia Europa… Será la primera vez que lideremos al mundo, por delante de EEUU. ¿Podremos? Ni de coña. La macro de la UE está birriosa…

PD2: Esto es lo que ha hecho EEUU durante sus muchos años de QE:

¿Será capaz Europa de hacer algo parecido? Ni de coña…

PD3: Mucha de la subida habida en la bolsa de EEUU viene de la mano de las recompra de acciones por parte de las propias empresas. Ha sido muy intenso. ¿Puede durar más? Ni de coña. Mira el ejemplo de IBM:

Y su deuda:

¿Qué sentido tiene que siga recomprando acciones en vez de pagar su deuda, o reducirla…? Absurdo… Pan hoy y mucha hambre mañana…

Esto es lo que se ha recomprado en acciones en EEUU:

¿Se han pasado? Sí, 20 pueblos… ¿Ves a las empresas europeas comprando sus propias acciones para que suban de precio, para que suba la cotización? Ni de coña…

PD4: La situación del mercado y de la macro no van parejas:

Y el problema deriva más este año de los beneficios de las empresas estadounidenses que se enfrían… Los de la UE siguen muy flojitos… Y en bolsa, al margen de expectativas, lo que se compran son beneficios de empresas…

¿Serán las europeas capaces de copiar la estela de fuertes beneficios que tuvieron las yanquis? Ni de coña…

Incluso alguno dice que esto es el preludio de una recesión en EEUU: tampoco es eso…, o sí???

PD5: Lo que ha cambiado en tan pocos años:

Esa supremacía de EEUU en la bolsa sobre todas las demás…

PD6: Además, en Europa tenemos un problema del sector bancario, y su peso es muy elevado en los índices:

PD7: Este joven sacerdote, Mike Schmitz, lo tiene claro: El confesionario es el lugar más alegre, humilde e inspirador del mundo. En él, veo actuar la preciosa misericordia de Dios, el poder transformador de su amor, y me recuerda qué bueno es Dios. Solemos intentar impresionar a los demás en muchas cosas de nuestra vida, pero la Confesión es un lugar donde no tenemos que impresionar a los demás. En el confesionario, el deseo de dar la talla muere. En la Confesión, encontramos a Jesús que nos recuerda: Eres digno de que yo muera por ti… incluso en tus pecados. Cada vez que alguien viene a confesarse, veo a una persona que es profundamente amada por Dios, y eso es todo lo que cuenta.